When the world feared the worst

Value investing is back with a vengeance.

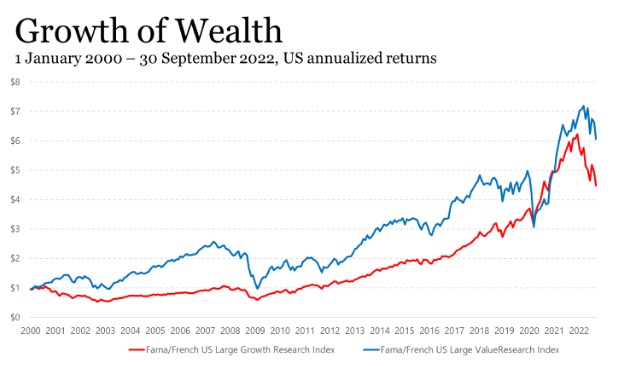

In the US share market, for the 21 months since January 2021, Value has out-performed Growth by 19.2% per annum.

A reminder what a Value company is – a company that is cheap compared to its assets. A Value company has perhaps been neglected by the market. It is not popular. And vice versa, a Growth company is expensive compared to its assets. Growth companies are typically popular companies where the price has been bid up compared to its assets.

The phwealth investment philosophy is based on scientific evidence supporting several style factors that demonstrate above-market investment returns over the long term. One of these style factors is ‘Value’. The evidence is that:

But not every year!

Explanation of the chart above:

What can we make of all this?

Despite the ten-year period from Jan 2011 to Dec 2020 showing Growth beating Value, over the past 23 years Value beat Growth by 1.5% per annum compound, see below:

As you can see, the really poor performance of Value compared to growth occurred during the Covid crash in February/March 2020. Tech companies, which are typically Growth companies, became very popular during the lockdowns as they provided the tools for commerce to continue. This reversed over 2021 and 2022.

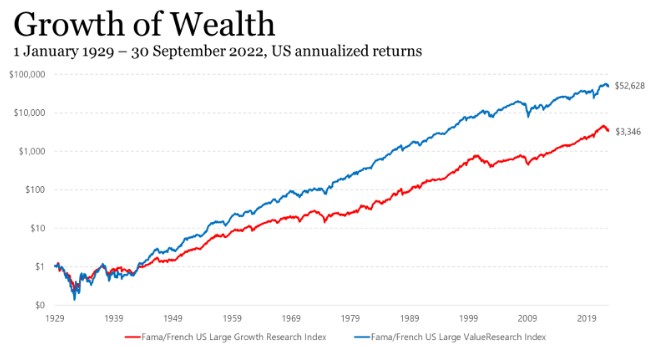

Over the very long term, we can see the compounding effect of the higher returns from Value in the graph below:

Over that time, $1 turned into $3,346 in large Growth companies while $1 turned into $52,628 in large Value companies.

Small Value companies have an even bigger edge, but that is for another time.

If you want to know more about our Value strategies, get in touch.

Keep asking great questions …